Marcel van Pinxteren. Manager Human Capital

Pension agreement: a battle between Finance and HR?

Last month we informed you in an article on this website about the financial impact of the Pension Accord on a company’s value.

In that article, we talked almost nothing about the pension to be achieved, the ambition level of the pension plan.

Of course, with a defined contribution plan, the starting point is often financial: what is the budget (read: the amount of the available premium) earmarked for accruing a retirement pension? The pension to be achieved is not leading. We notice in our “Pension Accord work” that the Pension Accord further emphasizes this. But let’s not forget that the basic purpose of retirement is to build wealth for later (read: retirement income)!

When determining the amount of the available premium, a balance will have to be sought between, on the one hand, the question of what budget the company is willing to release for the accrual of retirement pensions and, on the other hand, the question of what pension income a pension plan participant should reasonably achieve. In short, budget versus ambition level.

For the benefit of a fair number of our clients, we are now actively adjusting the existing pension building to the Pension Agreement. An important part of this is determining the level of the fixed available premium percentage on the basis of which the available premium intended for the accrual of old-age pension is determined. In this article, we share our experiences with you.

The impact analyses

The math should provide insight into the financial impact of the various scenarios and lead to informed decision-making on the part of the board. Of course, the pension policy must again be able to count on the approval of the Works Council and/or the employees concerned.

The computational work can be briefly summarized as follows:

- Step 1: Determining the fixed defined contribution rate on the basis of which the available premium intended to accrue retirement pension is determined.

- Step 2: Determine the financial impact of substantively harmonizing the existing progressive graduated scale with the proposed fixed rate.

- Step 3: Determining the compensation measure with respect to the resulting pension damage within the framework of the substantive harmonization described in Step 2.

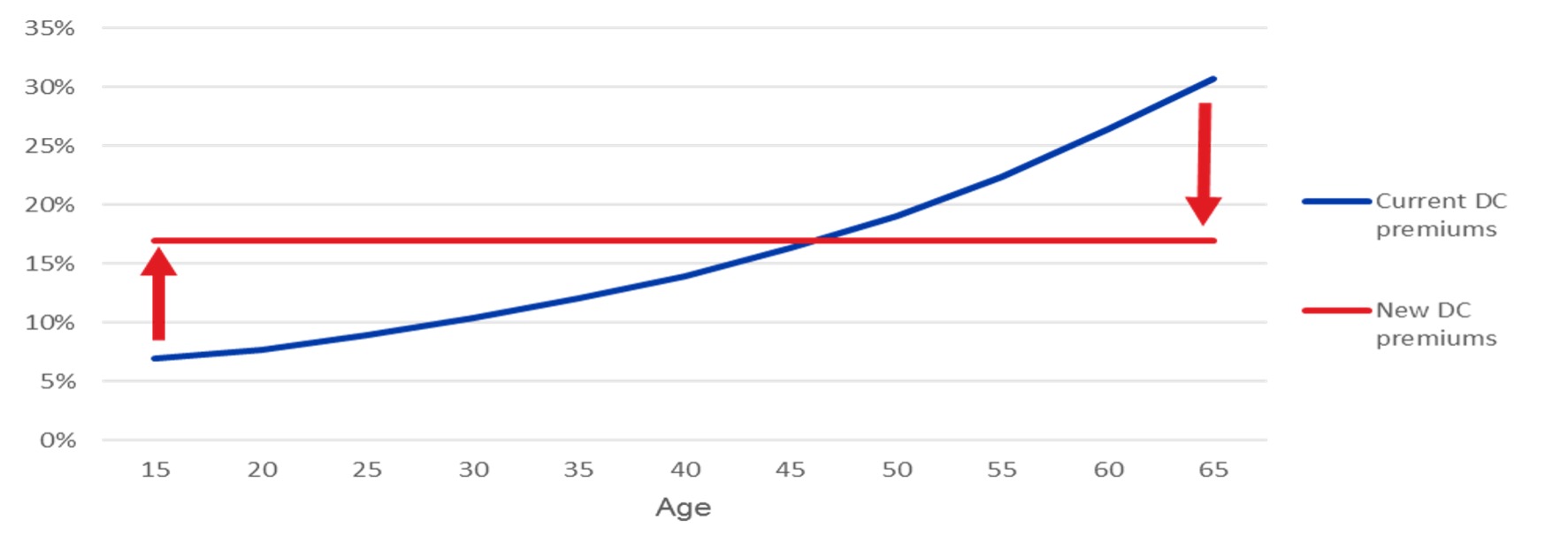

In the following, we assume an existing defined contribution plan, with a progressive defined contribution tier. Within such a graduated scale, available contribution rates increase with age, often in 5-year age cohorts.

The scenarios

Several scenarios are possible when determining the amount of the fixed available premium rate.

The available premium within the existing pension plan

The starting point is the existing pension plan. Based on the existing member base, the total amount of the available premium is determined and then expressed as a fixed percentage of pensionable earnings. This percentage is then maintained as the fixed available premium rate.

A few relevant points of interest:

- If the current pension plan is of a relatively low ambition level, this results in a relatively low fixed available contribution rate. This low rate produces a limited attainable retirement income.

- In this scenario, the amount of the fixed available contribution rate is derived from the existing participant base. It can be expected that the average age of the existing population is higher than the average age of the new employees to be recruited in the future. Should this be the case, the established fixed defined contribution rate for these new employees is “too high.

The level of ambition within the existing pension plan

Also in this scenario, the existing pension plan is the starting point. But with the level of ambition as the starting point. The ambition level represents the retirement income to be achieved. The calculation assumes a number of assumptions: an assumed rate of return and an assumed development of pensionable earnings during the accrual phase and an assumed actuarial interest rate on the retirement date.

One or more size people are calculated based on certain durations of employment. Consider:

- A participation rate over the total accrual period (18 years to 68 years)

- Employment from the average age at hire to the retirement guideline age (e.g., 27 years to 68 years)

- An expected tenure of new employees, based on the average age at hire (e.g., 27 years to 34 years).

The established ambition level associated with the selected scenario is then converted to a fixed available premium rate.

What are other employers doing?

In “the war for talent,” it is obviously good to know what other employers from one’s peer group or industry are doing.

It is common knowledge that employees pay relatively little attention to retirement benefits when choosing a new employer. However, it is expected that with the Pension Accord, more attention will be paid to this in the future.

After all, all pension plans are (no later than 01-01-2028) of the same type (a defined contribution plan), in which the pension premium intended to accrue a retirement pension is expressed as a fixed percentage. Comparing the fixed defined contribution rates maintained by the relevant employers within their pension plans is obvious.

Of course, the scenario of comparing with other employers is successful only if information is available from the other employers. At this stage of the transition period, however, this information is often still lacking: most employers are now working on their own pension file, but are not yet ready.

In that case, can’t it be redirected? One solution is to do go ahead and set the fixed available premium rate. Together, the employer and the Works Council, can additionally agree to benchmark the own percentage with the peer group or industry in a number of years (e.g. 3 years), when more market information is available, and adjust it when there is reason to do so. We also call this arrangement “the market conformity clause.

Fixed available premium rate determined and then?

And then once the percentage is determined, what is the next step? Then the important question of the pension policy to be adhered to arises:

- Substantively harmonize the existing defined contribution plan with mostly progressive tiers with the fixed rate plan? Result: a single pension plan for all employees, existing and new. But most likely complemented by a compensatory measure.

- Honoring the existing defined contribution plan with progressive tier for existing employees and the plan with fixed available contribution rate only for new employees? Result: a pension plan added.

There are advantages and disadvantages to both scenarios outlined above.

We will inform you further in our next newsletter (and on this website).

In the meantime, if you have any questions or need a personal consultation, we are of course always available for consultation: pensioenvragen@krollerboom.nl.

This article is posted by Marcel van Pinxteren. Manager of Human Capital

Do not miss our bulletins Sign up for the newsletter or follow us on LinkedIn

We will keep you up to date